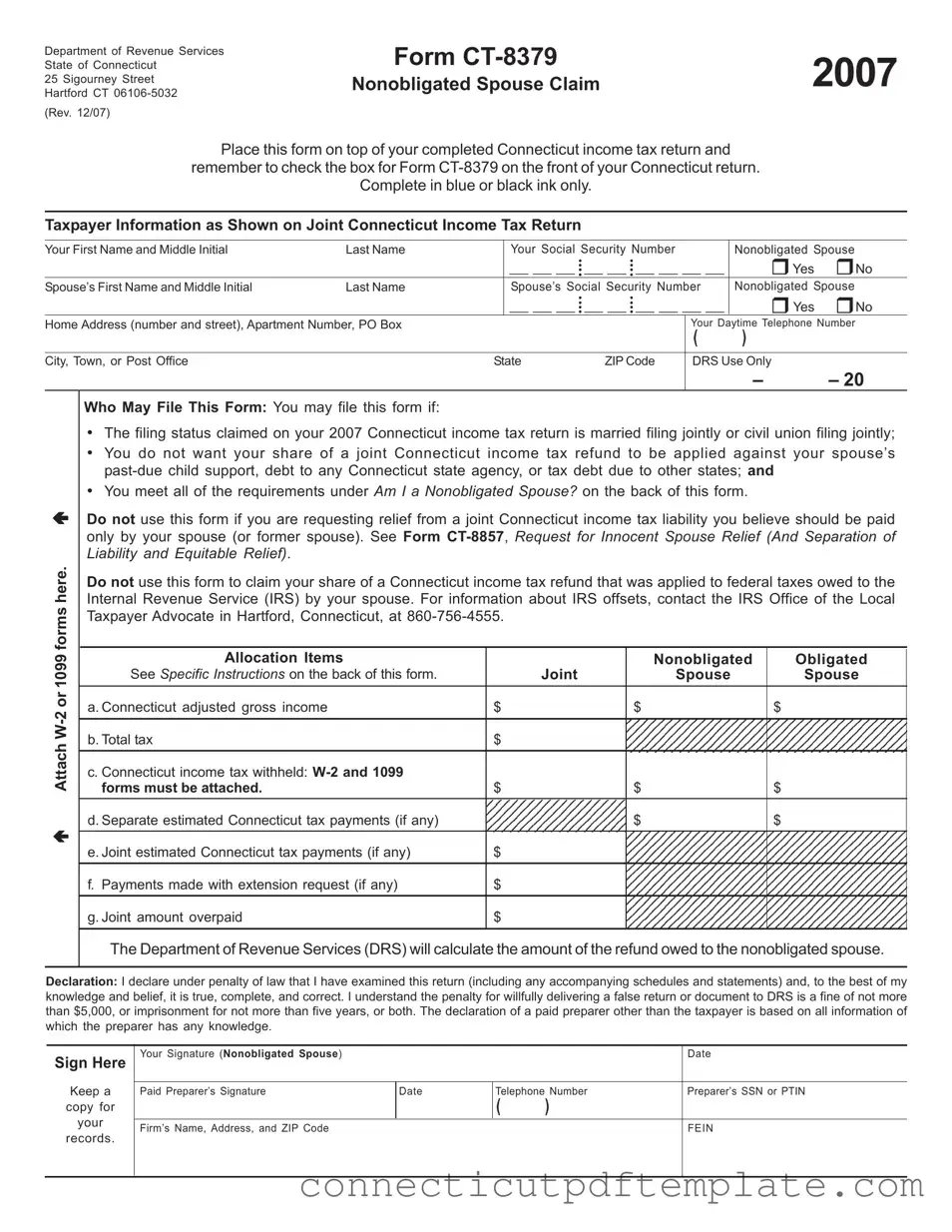

The Connecticut 8379 form, also known as the Nonobligated Spouse Claim, is an important document for couples filing their state income tax returns. This form is specifically designed for individuals who have filed a joint tax return but want to ensure that their portion of any tax refund is not applied to their spouse’s debts, such as past-due child support or other state obligations. To use this form, the taxpayer must meet certain criteria, including having filed jointly and having made income tax payments reported on that return. The form requires detailed information about both spouses, including names, Social Security numbers, and income allocations. It is crucial to attach relevant W-2 or 1099 forms to support the claims made. The Connecticut Department of Revenue Services will use the information provided to calculate the refund owed to the nonobligated spouse. Proper completion and submission of this form can help protect individuals from losing their rightful tax refunds due to their spouse's financial issues.

Department of Revenue Services

State of Connecticut

25 Sigourney Street

Hartford CT

(Rev. 12/07)

Form |

2007 |

Nonobligated Spouse Claim |

Place this form on top of your completed Connecticut income tax return and

remember to check the box for Form

Complete in blue or black ink only.

Taxpayer Information as Shown on Joint Connecticut Income Tax Return

Your First Name and Middle Initial |

Last Name |

|

Your Social Security Number |

|

Nonobligated Spouse |

|||

|

|

|

• |

• |

__ __ __ __ |

Yes |

No |

|

|

|

|

__ __ __ •• |

__ __ •• |

||||

|

|

|

• |

• |

|

|

Nonobligated Spouse |

|

Spouse’s First Name and Middle Initial |

Last Name |

|

Spouse’s Social Security Number |

|||||

|

|

|

• |

• |

__ __ __ __ |

Yes |

No |

|

|

|

|

__ __ __ •• |

__ __ •• |

||||

|

|

|

• |

• |

|

|

|

|

Home Address (number and street), Apartment Number, PO Box |

|

|

|

|

Your Daytime Telephone Number |

|||

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

City, Town, or Post Office |

|

State |

ZIP Code |

DRS Use Only |

|

|||

|

|

|

|

|

|

|

– |

– 20 |

Attach

Who May File This Form: You may file this form if:

•The filing status claimed on your 2007 Connecticut income tax return is married filing jointly or civil union filing jointly;

•You do not want your share of a joint Connecticut income tax refund to be applied against your spouse’s

•You meet all of the requirements under Am I a Nonobligated Spouse? on the back of this form.

Do not use this form if you are requesting relief from a joint Connecticut income tax liability you believe should be paid only by your spouse (or former spouse). See Form

Do not use this form to claim your share of a Connecticut income tax refund that was applied to federal taxes owed to the Internal Revenue Service (IRS) by your spouse. For information about IRS offsets, contact the IRS Office of the Local Taxpayer Advocate in Hartford, Connecticut, at

|

Allocation Items |

|

Nonobligated |

Obligated |

|

See Specific Instructions on the back of this form. |

Joint |

Spouse |

Spouse |

|

|

|

|

|

|

a. Connecticut adjusted gross income |

$ |

$ |

$ |

|

|

|

|

|

|

b. Total tax |

$ |

|

|

|

|

|

|

|

|

c. Connecticut income tax withheld: |

|

|

|

|

forms must be attached. |

$ |

$ |

$ |

|

|

|

|

|

|

d. Separate estimated Connecticut tax payments (if any) |

|

$ |

$ |

|

|

|

|

|

|

e. Joint estimated Connecticut tax payments (if any) |

$ |

|

|

|

|

|

|

|

|

f. Payments made with extension request (if any) |

$ |

|

|

|

|

|

|

|

|

g. Joint amount overpaid |

$ |

|

|

|

|

|

|

|

The Department of Revenue Services (DRS) will calculate the amount of the refund owed to the nonobligated spouse.

Declaration: I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return or document to DRS is a fine of not more than $5,000, or imprisonment for not more than five years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Sign Here

Keep a

copy for

your

records.

Your Signature (Nonobligated Spouse) |

|

|

|

Date |

|

|

|

|

|

Paid Preparer’s Signature |

Date |

Telephone Number |

Preparer’s SSN or PTIN |

|

|

|

( |

) |

|

|

|

|

|

|

Firm’s Name, Address, and ZIP Code |

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

Form

Purpose: Use Form

•You are a nonobligated spouse and all or part of your overpayment was (or is expected to be) applied against:

•Your spouse’s past due State of Connecticut debt (such as child support, student loan, or any debt to any Connecticut state agency); or

•A tax debt due to other states; and

•You want your share of the joint overpayment refunded to you.

Any reference in this document to a spouse also refers to a party to a civil union recognized under Connecticut law.

General Instructions

Am I a Nonobligated Spouse?

You are a nonobligated spouse, if you meet all of the following requirements:

•You filed a joint Connecticut income tax return with a spouse who owes

•You received income (such as wages, interest, etc.) reported on the joint return;

•You made Connecticut income tax payments (such as withholding or estimated tax payments) reported on the joint return;

•You do not owe

•You filed a joint return reporting an overpayment of Connecticut income tax, all or part of which was or is expected to be applied against

Filing the Return: You must file Form

You must place this form on top of the completed Connecticut income tax return. If you previously filed your 2007 Connecticut income tax return, mail this form separately to: Department of Revenue Services, PO Box 5035, Hartford CT

Important: Attach copies of all forms

showing Connecticut income tax withheld to Form CT- 8379.

Specific Instructions

Taxpayer Information: Enter the taxpayer information exactly as it appears on your Connecticut income tax return. The name and Social Security Number (SSN) entered first on the joint tax return must also be entered first on Form

Allocation Items

a.Connecticut adjusted gross income: Enter the joint amount as reported on your joint Connecticut income tax return (Form

Nonresidents and

Nonresidents and |

Connecticut Source Income |

|

(Form |

||

Only |

||

|

Allocation Item

Joint

Nonobligated Spouse

Obligated Spouse

b.Total tax: Enter the joint Connecticut tax liability as reported on your joint Connecticut income tax return (Form

c.Connecticut income tax withheld: Enter the joint Connecticut withholding as reported on your joint Connecticut income tax return (Form

d.Separate estimated Connecticut tax payments: Enter any separately paid estimated Connecticut income tax payments in the appropriate spaces.

e.Joint estimated Connecticut tax payments: Enter the total amount of any joint estimated Connecticut income tax payments. Include overpayments applied from a previous year.

f.Payments made with extension request: Enter the joint amount as reported on your joint Connecticut income tax return (Form

g.Joint amount overpaid: Enter the joint amount overpaid as reported on your joint Connecticut income tax return (Form

Nonobligated Spouse Refund: DRS will calculate the amount of the nonobligated spouse’s refund. The nonobligated spouse’s share of the joint Connecticut tax overpayment cannot exceed the joint overpayment.

Signature: The nonobligated spouse must sign this form.

Others Who May Sign for the Nonobligated Spouse: Anyone with a signed Power of Attorney may sign on behalf of the nonobligated spouse. Attach a copy of the Power of Attorney.

Paid Preparer’s Signature: Anyone you pay to prepare your return must sign and date it. Paid preparers must also enter their SSN or Personal Tax Identification Number (PTIN), and their firm’s Federal Employer Identification Number (FEIN) in the spaces provided.

Form

| Fact Name | Details |

|---|---|

| Form Purpose | Form CT-8379 is used by a nonobligated spouse to claim their share of a joint Connecticut income tax refund that may be applied against the obligated spouse's debts. |

| Filing Status | This form is applicable only if the couple's filing status is either married filing jointly or civil union filing jointly. |

| Eligibility Criteria | To qualify, the nonobligated spouse must meet specific conditions, including not owing any past-due debts that could affect the refund. |

| Required Attachments | W-2 or 1099 forms showing Connecticut income tax withheld must be attached to the form when submitted. |

| Governing Law | Form CT-8379 is governed by Connecticut General Statutes, specifically those related to tax refunds and obligations. |

| Submission Guidelines | The form must be placed on top of the completed Connecticut income tax return and should be filed with Form CT-1040, CT-1040EZ, CT-1040NR/PY, or CT-1040X. |

| Refund Calculation | The Connecticut Department of Revenue Services (DRS) calculates the refund amount owed to the nonobligated spouse based on the information provided. |

| Signature Requirement | The nonobligated spouse must sign the form. A paid preparer must also sign and provide their identification details. |

| Important Note | This form cannot be used to claim a share of a refund that has been applied to federal taxes owed by the obligated spouse. |

Web Reporting - A detailed guide on filling out the UC-2 is provided by state authorities to assist employers.

A Texas Quitclaim Deed form is a legal document used to transfer ownership of property from a seller to a buyer, typically with no warranty of title. This form is often utilized to transfer property between family members or to clear up title issues quickly. To securely transfer ownership rights in Texas, consider filling out the quitclaim deed form by visiting Texas PDF Forms for further assistance.

Connecticut Fpd 124 - Facilitates the creation of a detailed database of transactions, which can be instrumental in criminal investigations.